Despite Spike in Construction Costs, Cre Is Recovering Better Than Expected.

When COVID-19 changed work and home life at the end of the first quarter of 2020, commercial real estate sales and leasing activity slowed significantly due to the uncertainty. As the year progressed, market activity returned producing clear winners and losers - strength in the industrial, self-storage, and net-leased markets, worries in hospitality, retail, and office leasing markets. The pandemic exacerbated changes already taking place in the economy, such as e-commerce, ghost kitchens, and millennial homebuyers, which drove commercial real estate activity in 2020. Prices fell far less than after the 2008 financial crisis and are already rising again. Buyers/sellers and landlords/tenants are adjusting to the 'new normal' and transactions are closing - with some new concerns about the future.

Fear of inflation. Concerns about long-term inflation are top of mind as investors wonder if the sharp rise in recent months will prove transitory. While economic expansion continues to depend on interest rates and fiscal stimulus, it will ultimately be contingent on whether employers can find labor. Despite the Fed's insistence that rising costs are temporary - resulting from supply shortages and rapid reopening brought on by the pandemic - many CPG companies (like Kimberly-Clark, P&G, Coca-Cola) have already decided to pass these costs onto customers. Landlords and tenants in the commercial real estate space also seem to believe inflation will last, as leases with CPI clauses and rent escalations of 4-5% (versus the typical 2-3%) are readily being signed. Coldwell Banker Commercial professionals in a few leading markets are also seeing slight moderation in developer tempo from the beginning of the year due to soaring material costs. Amid all this market uncertainty, one thing is clear - both buyers and sellers have been acting quickly to get deals done before terms change.

More cap rate compression. Record amounts of sidelined money are returning to the market and finding very little product availability. While low-interest rates (rather than operating fundamentals) drove the decline in cap rates during the pandemic, there is still plenty of room for compression as frustrated buyers are now open to purchasing properties at much lower cap rates than they would have ever looked at before. With no wave of distressed properties materializing from this pandemic, sellers have the upper hand, forcing buyers to pay premiums on both opportunistic and long-term investments. This new surge of price increases could likely add to inflation.

Tolerance for risk is growing. When stock markets reach record highs, investors typically turn to real estate as an investment alternative that provides higher returns and a hedge against inflation. As the economic recovery gains steam, investors are showing a greater appetite for risk. The search for yield in a very low cap rate environment is pushing investors to new places, with many preferring secondary markets over the primary. Sunbelt states continue to be the most appealing, offering yields that can be 75 to 100 basis points higher than many gateway cities. We are also seeing renewed interest in highly-delinquent properties like B & C malls and small office space while robust demand for multifamily, logistics & storage, medical office, QSR and grocery-anchored retail continues.

1031 exchanges. The uncertain future of the 1031 exchange (an extremely popular tool during the pandemic) has created another surge in demand for replacement properties as well as a huge sense of urgency to close deals quickly. Adverse changes or elimination from the current tax code could lead to billions in lost property value for many small investors and potentially freeze capital. Assets under $10 million are seeing strong interest, with buyers focusing on properties that can close quickly - such as warehouses, distribution facilities, and single-tenant retail stores leased to essential businesses with long lease terms. Exchange investors are avoiding apartment buildings, multi-tenant retail centers, and properties that require more day-to-day management.

Office space in transition. The pandemic has caused major shifts, with big corporations shying away from typical 7-10 year renewals as they figure out how they want to use the space. While businesses found that they can be productive with employees working from home, 70% of CEOs want people to return to the office (according to staffing firm LaSalle Network). Over half of office workers, however, would prefer to be remote at least part of the time - vaccinated or not - and say they would leave their job if it didn't offer a hybrid solution. With so much uncertainty in the market, most occupiers are looking for short-term lease obligations, mainly in the 1-3 year range with options. There is no standard approach right now, as many companies are evaluating what roles need to come in and what configurations best suit 2-3 days in-office a week. With no solid return plans in place, the next 9- 12 months will likely see vacancy rates rise significantly.

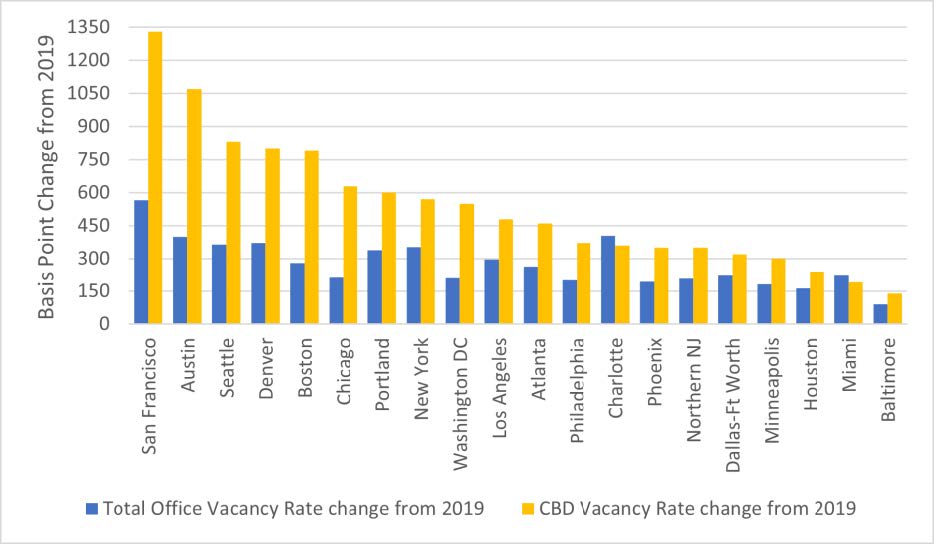

Exhibit 1: Top-20 Office Markets: Total Vacancy vs. CBD Vacancy Rate Change

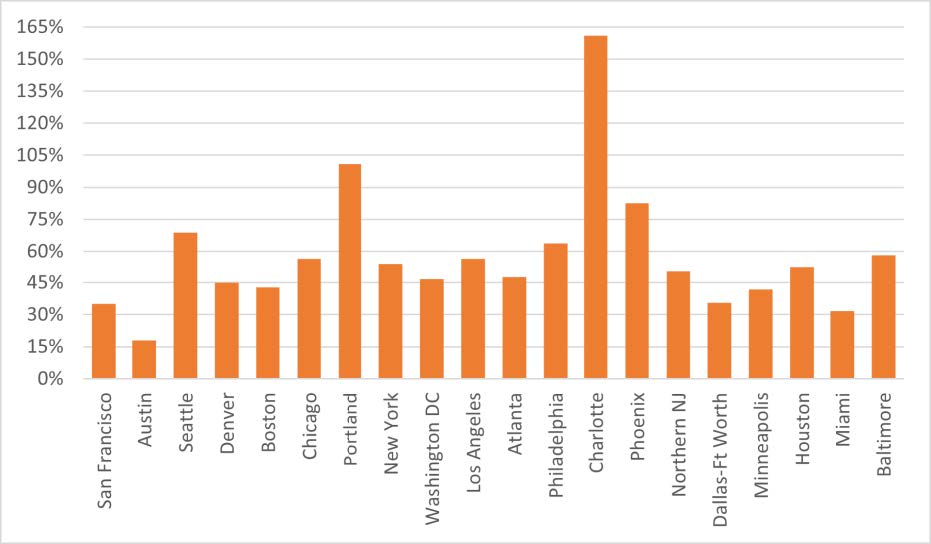

Exhibit 2: Top-20 Office Markets: YoY Percent Increase in Sublet Availability

Demand for small offices & collaboration space. While Class A buildings account for the majority of demand losses over the past year, the opposite holds true for mid-and lower-tier office products. Coldwell Banker Commercial professionals have seen frenetic demand for small spaces (under 10,000 square feet) from all types of users - new enterprises, cryptocurrency traders, medical offices, labs, and professional service providers. The majority are owners/users while the balance consists of multi-tenant operators and high-net-worth investors looking to buy the building. Coworking space providers are also seeing an uptick in demand, as their ability to offer flexible leases has become a major strength at a time when big corporations are looking to implement a hub-and-spoke model. Traditional landlords will have to offer enticing amenities to get workers to come in. The question is what will owners and employers provide? The building that succeeds will be those that satisfy the needs of the tenant: more collaboration space, improved ventilation, touchless technology, catered lunches, gyms, childcare, on-site dry cleaning, and easy parking.

Retail will be all about repurposing. While America remains overstored, the economic recovery is bringing interest back to sit-down restaurants and local retailers who were able to pivot into online sales and curbside delivery during the pandemic. Coldwell Banker Commercial-affiliated professionals across the country are seeing a pickup in bank lending for these neighborhood retail properties. Restaurant bookings to date are up 48%, ahead of pre-pandemic levels in every state but New York (according to Yelp). On the flip side, developers have been eyeing malls hard-hit by the pandemic for conversion to mixed-use residential space. While not a new concept, the acceleration of mass store closures and lease terminations open opportunities for larger-scale master planning. New occupiers will likely give prominence to the live-work-play idea and could include entertainment venues, healthcare clinics, ghost kitchens, cannabis dispensaries, distribution facilities, and e-commerce warehouses. How high will conversion costs go given the dramatic increases in building materials and labor shortages?

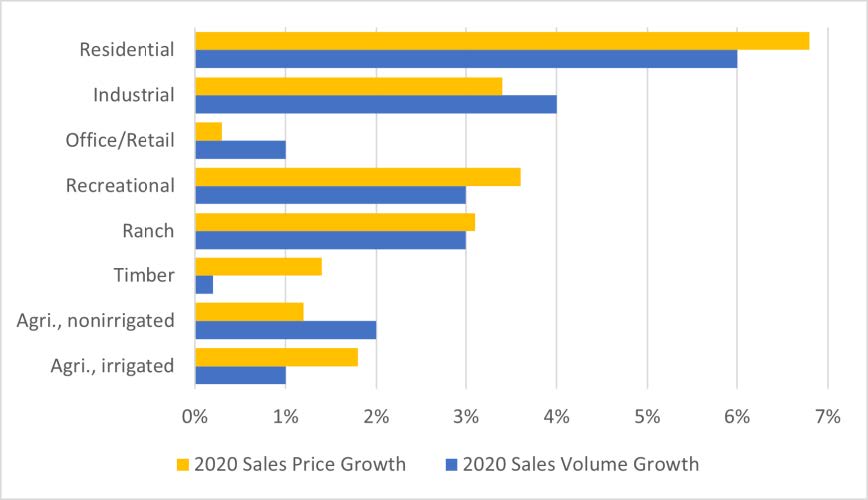

Exhibit 3: YoY Percent Growth in Land Sales, Led by Residential and Industrial

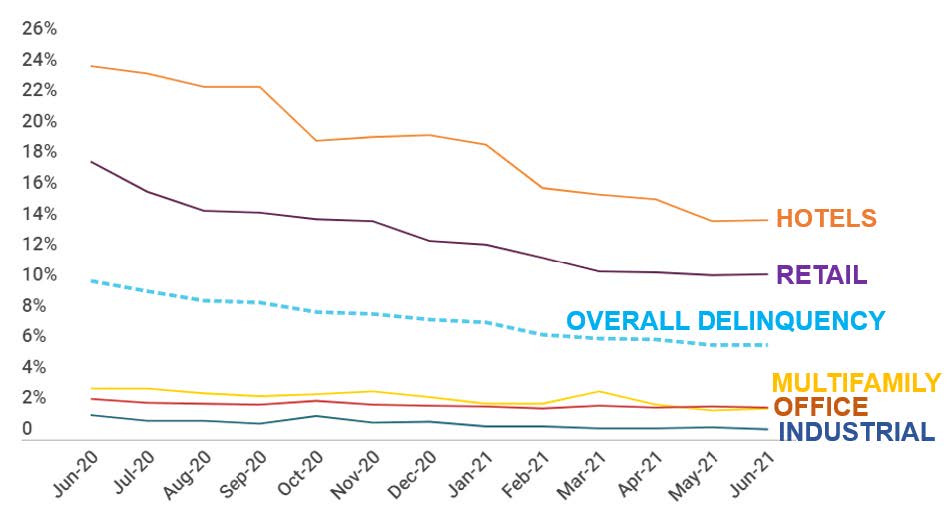

Exhibit 4: Month-over-Month Delinquency Rates by Property Type